Introduction

The Petrochemicals Market encompasses the production, distribution, and utilization of chemical products derived from petroleum and natural gas feedstocks. These compounds — including ethylene, propylene, butadiene, benzene, toluene, and xylene — serve as foundational building blocks for plastics, synthetic rubbers, solvents, fibers, coatings, adhesives, and other essential materials. As global industrialization, infrastructure development, and consumer product demand continue to rise, petrochemicals remain integral to manufacturing, automotive, packaging, construction, and electronics sectors.

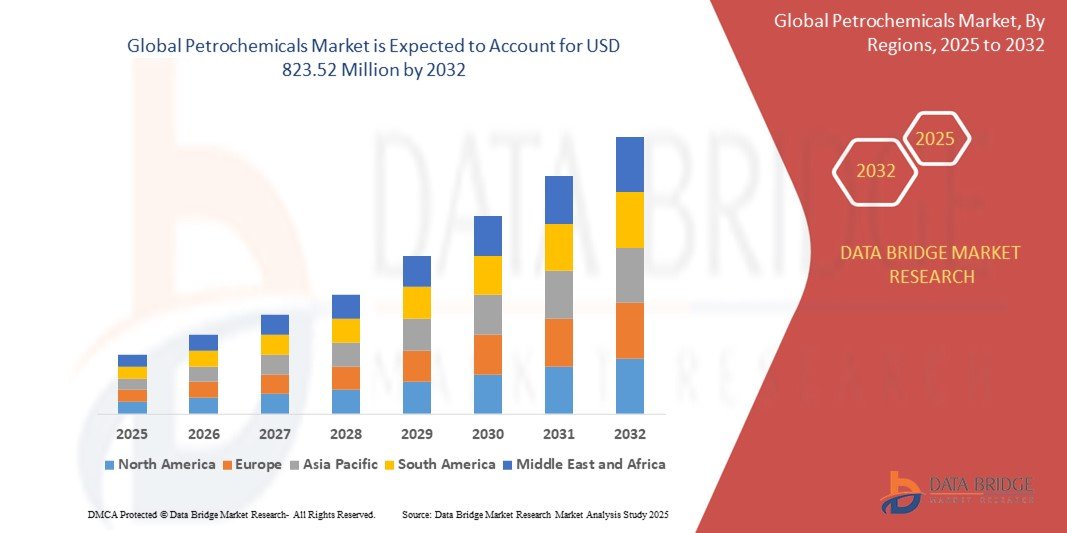

Market Size and Growth Projections

The petrochemicals market has shown substantial growth historically and is expected to maintain a steady compound annual growth rate over the forecast period. This expansion is supported by rising production capacities in emerging economies, robust demand from end-use industries, and ongoing investments in downstream processing technologies. Growth in packaging materials, automotive components, and consumer goods continues to drive demand for fundamental petrochemical derivatives.

Get More Details : https://www.databridgemarketresearch.com/reports/global-petrochemicals-market

Key Growth Factors

- Increasing demand for plastics, resins, and synthetic materials

- Expansion of manufacturing and construction activities worldwide

- Growth in automotive and aerospace sectors

- Rising use of petrochemicals in packaging and consumer products

- Investments in advanced refining and petrochemical integration

Market Segmentation

By Product Type

- Olefins (Ethylene, Propylene)

- Aromatics (Benzene, Toluene, Xylene)

- Synthetics (Butadiene, Styrene)

- Others

Olefins represent a dominant share due to extensive use in polyethylene, polypropylene, and other commodity polymers.

By Feedstock

- Naphtha

- Natural Gas Liquids (NGLs)

- Others

Naphtha continues to be a primary feedstock in regions with established refining complexes, while NGL feedstocks grow in markets with abundant shale gas resources.

By Application

- Plastics & Polymers

- Synthetic Rubber

- Solvents & Intermediates

- Coatings & Adhesives

- Fibers & Textiles

- Others

Plastics and polymers hold the largest application share due to broad usage in packaging, automotive parts, consumer goods, and industrial components.

By End User

- Packaging

- Automotive & Transportation

- Construction

- Consumer Goods

- Electronics & Electrical

- Industrial Equipment

Packaging remains a leading end-use segment as demand for flexible, lightweight, and recyclable materials increases globally.

Regional Insights

Asia-Pacific dominates the petrochemicals market due to rapidly expanding manufacturing sectors, large population base, and strategic investments in refining and petrochemical capacities. North America follows with substantial shale gas feedstock availability and integrated petrochemical complexes. Europe exhibits stable demand supported by specialty chemicals growth and advanced industrial infrastructure. Emerging regions such as Latin America and the Middle East & Africa present growth opportunities as industrial production expands.

Key Market Drivers

The market is propelled by the need for versatile and cost-effective chemical intermediates used in essential industries. Increasing demand for packaging materials, lightweight automotive components, and performance-enhancing additives fuels petrochemical consumption. Ongoing urbanization, infrastructure projects, and expanding consumer markets contribute to sustained market momentum.

Market Challenges and Restraints

Challenges include feedstock price volatility, environmental concerns related to plastic waste, regulatory pressure on petrochemical emissions, and fluctuating crude oil prices. The shift toward sustainable materials and circular economy principles may influence long-term demand for conventional petrochemicals. Investments in recycling and bio-based alternatives present both opportunities and competitive pressures.

Competitive Landscape with Key Companies

- BASF SE

- ExxonMobil Chemical

- Royal Dutch Shell

- SABIC

- Dow Inc.

- LyondellBasell Industries

- Chevron Phillips Chemical

- INEOS Group

Leading companies focus on capacity expansions, process optimization, strategic partnerships, and sustainability initiatives to enhance market positioning.

Technological Innovations

Technological advancements include process intensification, catalytic efficiency improvements, digital process optimization, and energy recovery systems. Innovations in chemical recycling, bio-based feedstocks, and advanced polymer formulations are reshaping product portfolios. Data analytics and automation improve operational efficiency, reduce costs, and enhance product quality.

SWOT Analysis

| Strengths | Weaknesses |

|---|---|

| Wide range of industrial applications | Feedstock price and supply volatility |

| Strong global demand for plastics and chemicals | Environmental and regulatory pressures |

| Established manufacturing infrastructure | High capital expenditure requirements |

| Opportunities | Threats |

|---|---|

| Growth in emerging industrial markets | Economic downturn impacting demand |

| Advancement in recycling and sustainability | Competition from bio-based alternatives |

| Investments in downstream integration | Geopolitical instability affecting supply |

Future Market Outlook

The petrochemicals market is expected to grow steadily as global manufacturing and consumer demand expand. Continued investments in advanced refining, feedstock diversification, and sustainability frameworks will shape future growth trajectories. Adoption of circular economy initiatives and chemical recycling technologies will further influence market dynamics.

Conclusion

The Petrochemicals Market remains a cornerstone of global industrial development, supplying fundamental materials for diverse sectors. As demand for plastics, synthetic materials, and chemical intermediates continues to rise, petrochemicals will maintain a central role in manufacturing value chains. Balancing growth with sustainability initiatives and technological advancements will define the future of the market.